Beyond Generative AI: Where the Next AI Investment Wave Is Forming

We all have seen how generative AI tools have attracted worldwide attention and billions of dollars in investment over the past few years. Chatbots, coding assistants, text-to-image tools, and AI copilots have become common productivity tools.

Foundation model companies attracted massive capital in 2025, raising $80 billion, accounting for 40% of all global AI funding. OpenAI and Anthropic together accounted for 14% of worldwide venture investment.

Now, the first phase of the AI era is maturing. This prompts a question from technologists and investors: where will the next wave of AI investment emerge?

Generative AI is still in its early stages, but the next major wave of investment is forming across several new sectors. A new group of AI investment categories is emerging, where systems act independently, physically exist in the real world, operate within regulated industries, and run with extreme efficiency at the cutting edge of computing.

Understanding the emerging AI shifts is crucial, as they also determine where the biggest financial gains of the next decade will be located.

The End of the “Generative AI Only” Phase

Generative AI has already changed the world. The success of ChatGPT, Claude, and other tools reflected how large foundation models would assist in text, images, code, video, and other digital assets.

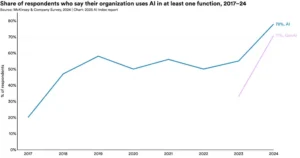

By 2025, 78% of organizations report using AI in some way, up from 55% in 2023, according to McKinsey. The number of companies utilizing generative AI in at least one business function more than doubled, from 33% to 71% within a year. These are remarkable adoption rates by any historical measure.

Despite all that, the enterprise-wide financial impact remains elusive. Only around 6% of organizations surveyed by McKinsey qualify as “AI high performers”. The rest are experimenting/deploying and struggling to convert AI returns. This gap between adoption and impact is why investors are looking beyond the generative layer.

Besides that, generating AI has limitations:

- High computing and energy costs

- Hallucination and reliability challenges

- Limited real-world interactions

- Heavy dependence on centralized cloud infrastructure

Furthermore, training large AI models can consume tens of gigawatt-hours of energy, underscoring the scalability challenges of current architectures. These limitations are another reason investors are shifting their focus toward systems that take AI applications beyond content creation to real-world intelligence.

Statistics show that global enterprise AI investment is expected to reach $632 billion by 2028. However, the nature of that investment is evolving. The trend is shifting from funding the base model layer, such as large language models, to investing in systems that incorporate those models into more autonomous and impactful architectures.

The next wave of AI innovation is focused on:

- Intelligence embedded in devices

- Autonomous decision-making systems

- Physical robotics and automation

- AI infrastructure and chips

- Domain-specific AI solutions

Let’s now get deep into the AI investment landscape beyond generative AI and highlight where the next generation of transformative opportunities is emerging.

The Four Frontiers of the Next AI Wave

1. Agentic AI — Chatbots to Digital Employees

If generative AI gave machines a voice, agentic AI gives them agency. Agentic systems do more than just respond to prompts. They plan, reason, take sequences of actions, and execute complex workflows with minimal human intervention. They can browse the web, write and run code, manage files, send emails, and coordinate with other agents to accomplish multi-step business goals.

The financial stakes are extraordinary. The global AI agent market is projected to grow from $7.92 billion in 2025 to $236 billion by 2034, at a compound annual growth rate of 45%.

Gartner predicts that 40% of enterprise applications will use task-specific AI agents by 2026, compared to less than 5% in 2025.

We have found this investment thesis compelling for several reasons:

- Agentic AI is disrupting traditional software unit economics. Instead of per-seat SaaS licensing, next-generation AI platforms are charging based on outcomes. They charge based on resolving a customer support ticket, generating a qualified sales lead, completing a compliance review, etc. This outcome-based pricing model aligns vendor and customer incentives in ways that traditional software never could, and it unlocks higher revenue potential per deployment.

- The enterprise adoption signals are accelerating. According to a PwC AI Agent Survey from 2025, 35% of organizations report broad adoption of AI agents, 27% have limited adoption, and 17% have fully implemented agents company-wide. Customer service is the initial beachhead, as CB Insights data shows 82% of organizations plan to use AI agents in customer support within 12 months. Besides that, the technology is spreading into finance, legal, healthcare administration, and software development.

The investment landscape in agentic AI is following into two categories:

- Horizontal Enterprise Agents: These agents serve cross-functional needs (coding, IT operations, knowledge management).

- Vertical Enterprise Agents: These are industry-specific agents that go deep into a single sector’s workflows.

Both represent significant opportunities, but vertical agents may offer stronger moats, since their value compounds through domain-specific data and integrations that are difficult for generalist competitors to replicate.

2. Physical AI and Robotics — Intelligence Embodied

The most dramatic frontier may be the one furthest from a screen. Physical AI refers to the integration of advanced machine intelligence with robotic systems, autonomous vehicles, drones, and smart infrastructure. It is becoming an operational reality in 2026, and the capital following it is beginning to reflect that.

Boston Dynamics’ Atlas humanoid robot began its first field test at a Hyundai manufacturing facility in Georgia in January 2026.

NVIDIA CEO Jensen Huang has declared that his company has achieved a “ChatGPT moment“ for physical AI, and the company’s Isaac and GR00T foundation models are positioning it as the operating system layer for next-generation robotics.

The data on enterprise adoption is striking. According to Deloitte’s State of AI in the Enterprise survey, 58% of organizations are already using physical AI to some extent. The adoption is expected to reach 80% within two years. Robotics ranks as the second most impactful form of physical AI for enterprise innovation, only behind intelligent security and monitoring systems. The top deployment sectors are manufacturing, logistics, and defense.

The investment opportunity in physical AI is layered. At the infrastructure level, NVIDIA’s Isaac Sim and Omniverse platform provide the simulation environment needed to train robots. At the application level, humanoid robotics companies, autonomous vehicle platforms, agricultural robotics, and surgical automation systems reflect distinct verticals, each with its own development timeline and capital requirements.

The long-term impact of physical AI is hard to overstate. Nearly $100 billion is expected to be invested in sovereign AI compute by 2026, according to World Economic Forum analysis. Governments are viewing physical AI infrastructure as a matter of national competitiveness. Watch as intelligence moves from the cloud into the physical world—factories, hospitals, roads, and homes. When that happens, the addressable market becomes the entire built environment.

3. Vertical AI — The Deep Specialization Premium

Another strong investment theme emerging in the post-generative era is the value of deep domain expertise. General-purpose AI models are becoming commoditized more quickly. The performance gap between the top closed models and the best open-weight alternatives shrank from 8% to just 1.7% on certain benchmarks within a year. Hardware costs have decreased by 30% annually, while energy efficiency has improved by 40% each year.

Today, the focus is switching toward owning a better model trained on proprietary data and integrated with industry-specific workflows, along with being embedded in regulatory and compliance infrastructure. This is the thesis behind vertical AI, and investors are well convinced by it.

Consider healthcare as an example. AI systems trained on medical datasets are now capable of assisting doctors in diagnosing diseases. They can even help recommend treatment plans. The global healthcare AI market is projected to exceed $188 billion by 2030, which reflects strong demand for specialized clinical tools. Because these platforms combine domain expertise, regulatory compliance, and high-value data, they are far harder to replicate than general AI models. That’s the reason why vertical AI startups in healthcare, finance, legal services, and other industries are attracting significant investor interest.

Bessemer Venture Partners, in its 2025 State of AI report, identified vertical AI as one of the most compelling categories for venture investment. The strongest companies are moving well beyond model fine-tuning and into verticalized utility. The firms winning in vertical AI are delivering “10x productivity” gains that are immediately legible to customers, with no complex ROI calculation required.

4. AI Infrastructure 2.0 — Beyond the GPU

The first wave of AI infrastructure was about more compute, better AI. Microsoft, Alphabet, Amazon, and Meta spent a combined over $300 billion on AI infrastructure in 2025 alone. That money built a lot of data centers and made a lot of chip designers very wealthy. But raw compute is no longer the bottleneck.

The next wave of infrastructure focuses on what surrounds the model, such as memory, governance, orchestration, and energy systems that determine whether AI functions reliably in the real world.

Governance is a key area in this shift that attracts investment. The World Economic Forum found that only 21% of enterprise leaders have a mature governance model for autonomous agents. Since agentic AI is taking on higher-stakes decisions, that gap is becoming a serious liability and a significant commercial opportunity.

Energy is becoming harder to ignore. Data centers use a large share of the world’s electricity. Microsoft has already restarted the Three Mile Island nuclear plant to meet demand. Google and Amazon have taken similar actions. The issue of AI energy consumption is real, and addressing it is creating some of the most interesting infrastructure investment opportunities outside of traditional tech.

Finally, edge AI is also gaining significant momentum. It involves running models directly on devices instead of in the cloud. When smaller and faster models run on smartphones and industrial equipment or sensors, they avoid latency and privacy issues.

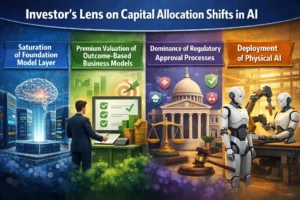

Investor’s Lens on Capital Allocation Shifts in AI

The shift beyond generative AI has direct implications for how capital should be allocated over different time horizons and risk profiles. Several principles stand out in the current investment scenarios.

Saturation of Foundation Model Layer

First, the foundation model layer is nearing saturation. Since the two largest model companies alone account for 14% of all global venture investment in 2025, the performance of the models converges regardless of who built the underlying system. Therefore, the marginal return on additional foundation model investment is decreasing. The next dollar invested in base model capability is less likely to produce outsized returns than the next dollar invested in the application and agentic layers built on top of those models.

Premium Valuation of Outcome-Based Business Models

Second, outcome-based business models warrant a valuation premium. Companies that charge based on completed tasks rather than software seats demonstrate a different connection between AI capability and revenue. As agentic systems improve, these companies’ revenue per customer increases automatically. Investors who grasp this distinction will be better equipped to assess high valuations in the agentic AI sector.

Dominance of Regulatory Approval Processes

Third, there is a growing focus on regulatory-approved processes. Think healthcare, finance, legal work, or government contracts. AI companies that navigate approvals, establish strong compliance systems, and build trust with major institutional clients have a significant advantage that’s hard to beat. The key insight here is that the most valuable positions in vertical AI may not be the most technically innovative companies but those that have done the most challenging institutional work.

Deployment of Physical AI

Fourth, physical AI is a long-term gamble that is becoming shorter. The deployment of humanoid robots in commercial manufacturing by early 2026 signals their economic usefulness. The investment timeline for physical AI remains measured in years, but the turning point is coming faster than many anticipated.

Conclusion

Generative AI triggered the latest surge in artificial intelligence investments, but it is only the start of a much larger transformation. The upcoming wave of AI investment is forming across various fields, as mentioned earlier. These technologies will push AI beyond content creation and into the essential systems that drive the global economy. The investors who will shape the next decade are those who can identify where generative AI ends and where the next frontier begins.